Do you feel like your salary disappears every month? Many people face this problem because they don’t have a clear plan for their money. This is where zero based budgeting can help. It is a simple method where every rupee is assigned a purpose, so you always know where your money is going.

Most people don’t have a money problem. They have a planning problem. You earn, you spend, and at the end of the month, you wonder where everything went. If this sounds familiar, then this guide is for you.

In this blog, we will understand zero based budgeting in a very simple way, with real-life examples that you can actually relate to.

What is Zero-Based Budgeting?

Zero based budgeting is a way of planning your money where your total income is completely assigned to different categories like expenses, savings, and investments.

At the end of your budget, the balance becomes zero. This does not mean you spend all your money. It simply means every rupee has a job.

Instead of leaving money unplanned, you decide in advance where it should go. This gives you clarity and control.

For example, if your monthly income is ₹30,000, you will divide this amount into rent, food, travel, savings, and other needs in such a way that the total becomes ₹30,000. Nothing is left without purpose.

Why Most People Struggle Without a Budget

Before understanding how this method works, it is important to see why people struggle with money.

Most people spend based on habits, not planning. Small expenses like online orders, subscriptions, and random purchases slowly add up. Since there is no tracking, money gets used without awareness.

Another reason is that people think they will save whatever is left at the end of the month. In reality, nothing is left.

This is why zero based budgeting is powerful. It forces you to plan first and spend later.

How Zero-Based Budgeting Works

The idea is very simple. You take your total income and assign it fully.

Let’s say your monthly income is ₹30,000.

Now instead of spending randomly, you plan it like this:

You keep ₹10,000 for rent, ₹5,000 for food, ₹2,000 for travel, ₹3,000 for bills, ₹5,000 for savings, ₹3,000 for emergency fund, and ₹2,000 for personal spending.

When you add all of this, it becomes ₹30,000.

Now your budget is complete. There is no confusion and no guessing.

This method makes you think before spending because every rupee is already planned.

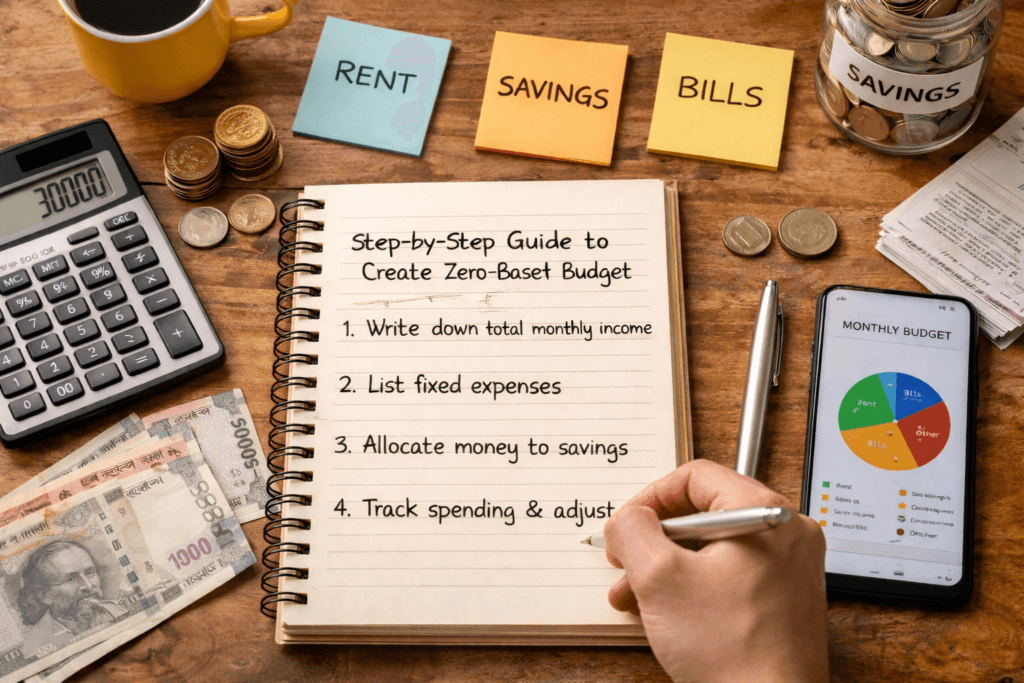

Step-by-Step Guide to Create Zero-Based Budget

You don’t need any special knowledge or tool to start. You just need a notebook or even your phone notes.

First, write down your total monthly income. Be clear about how much you actually receive after deductions.

Next, list all your fixed expenses like rent, electricity bill, mobile recharge, and groceries. These are the basic needs that you cannot avoid.

After that, think about your savings. This is where most people make mistakes. Savings should not come later. It should be planned first.

Then assign amounts to each category carefully. Make sure your total income is fully distributed.

Finally, track your spending. If you spend more in one area, adjust somewhere else. Budgeting is not about perfection. It is about awareness.

Real Life Example of Zero-Based Budgeting

Let’s take a simple real-life example.

Amit is a working professional earning ₹30,000 per month.

Earlier, he had no budget. By the 20th of every month, he used to feel stressed because his money would almost finish. He had no savings and often borrowed small amounts from friends.

Then he decided to try zero based budgeting.

He planned his salary like this:

₹10,000 for rent

₹5,000 for food

₹2,000 for travel

₹3,000 for bills

₹4,000 for savings

₹3,000 for emergency fund

₹3,000 for personal use

Now his full ₹30,000 was planned.

In the first month itself, he noticed a big change. He stopped ordering food unnecessarily. He avoided small wasteful expenses. Most importantly, he was able to save money for the first time.

After three months, he had built a small emergency fund. This gave him confidence and peace of mind.

This is how small planning can create big change.

If you are struggling to save money every month, you can also check our guide on how to save money on low income.

Benefits of Zero-Based Budgeting

One of the biggest benefits of this method is clarity. You always know where your money is going. There is no confusion.

It also helps you control spending. Since everything is planned, you think twice before making unnecessary purchases.

Another benefit is better savings. When you plan your savings in advance, you don’t skip it.

It also builds discipline. Over time, you develop better financial habits without even realizing it.

Most importantly, it works for everyone. Whether your income is small or big, this method can be applied easily.

Challenges You May Face

Like any method, zero based budgeting also has some challenges.

At the beginning, it may feel time-consuming. You may feel confused about how much to assign to each category.

Sometimes unexpected expenses can disturb your plan. For example, sudden medical expenses or travel.

Also, if you don’t track your spending regularly, the budget may not work properly.

But these challenges are temporary. Once you get used to it, budgeting becomes a natural habit.

Who Should Use Zero-Based Budgeting?

This method is very useful for beginners who are just starting to manage their money.

It is also helpful for people who feel their expenses are out of control.

If you are someone who struggles to save money, this method can be very effective.

Even salaried employees with fixed income can benefit a lot because it helps in planning monthly expenses properly.

Zero-Based Budgeting vs 50/30/20 Rule

You may have heard about another popular method called the 50/30/20 rule.

In that method, you divide your income into three parts. Fifty percent goes to needs, thirty percent to wants, and twenty percent to savings.

This method is simple and easy to follow.

But zero based budgeting is more detailed. It gives you more control because you assign every rupee.

If you prefer simplicity, you can go with the 50/30/20 rule. But if you want better control and awareness, zero based budgeting is a better option.

To understand a simpler budgeting approach, check out our guide on the 50/30/20 budget rule for beginners with example.

Common Mistakes to Avoid

Many people start budgeting but give up quickly. This usually happens because of small mistakes.

One common mistake is not tracking expenses regularly. Planning is not enough. You must also monitor your spending.

Another mistake is setting unrealistic budgets. If your plan is too strict, you may not follow it.

Ignoring small expenses is also a problem. Small daily expenses can add up to a big amount.

Lastly, not reviewing your budget every month can make it ineffective. Your income and expenses may change, so your plan should also change.

Simple Tips to Make It Work

Start with a simple plan. Don’t try to make it perfect from day one.

Be honest with your expenses. Write everything clearly.

Review your budget weekly so you can adjust early if needed.

Stay consistent. The real benefit comes when you follow this method for a few months.

Final Thoughts

According to official financial awareness initiatives by the Government of India, managing your money through proper budgeting is an important step towards financial stability.

Zero based budgeting is not just a financial method. It is a habit that can change the way you think about money.

It helps you move from confusion to clarity. Instead of wondering where your money went, you start deciding where it should go.

Even if your income is small, proper planning can make a big difference.

If you are serious about improving your financial life, start using zero based budgeting today. Over time, you will see how small decisions can lead to big results.

For more helpful tips like this, explore our Personal Finance guides where we cover budgeting, saving, salary, and money management in simple ways.

FAQs

What is zero based budgeting in simple words?

Zero based budgeting means planning your income in such a way that every rupee is assigned a purpose. Instead of spending first and saving later, you decide in advance where your money will go.

Is zero based budgeting good for beginners?

Yes, zero based budgeting is very useful for beginners. It helps you understand your expenses clearly and gives you better control over your money from the start.

Can I save money using zero based budgeting?

Yes, you can save money easily using this method because savings are included in your plan from the beginning. This ensures you don’t skip saving at the end of the month.

Is zero based budgeting difficult to follow?

It may feel a little difficult in the beginning, especially when you are not used to tracking your expenses. But once you follow it for a few weeks, it becomes simple and natural.

Which is better, 50/30/20 or zero based budgeting?

The 50/30/20 rule is simpler and easier to follow, while zero based budgeting gives you more control over your money. If you want detailed planning, zero based budgeting is a better option.

Disclaimer

This article is for informational purposes only and does not provide financial advice. Please consult a financial advisor before making any financial decisions.

Amit Singh is an experienced IT professional and passionate blogger with 8+ years in the technology industry. Through Resource Locator, he shares practical finance strategies, productivity tips, and useful technology insights to help readers make smarter everyday decisions.